20.04.2022 - Studies

What is a small thing for one person can be a big deal for another - this is true in real life as well as in business relationships. This is the case for Rossell India, for example. On the one hand, the company produces tea; on the other, it offers solutions for electronic systems and cable harnesses. And that's where the Indians got into business with Boeing. Rossell recently made almost 5.3 million dollars in quarterly sales with the US aviation giant. For Boeing, that was a mere 0.03 per cent of quarterly costs. For Rossell India, on the other hand, it was enough to secure its existence: the business represented 48.4 per cent of its total revenues in the quarter.

How deeply entrenched the partnership between Rossell and Boeing is remains to be seen. For it is not only since Russia's war of aggression on Ukraine that the global division of labour that has been promoted for decades has been called into question. The Corona pandemic has already shown the vulnerability of global supply chains. Now the word deglobalisation is doing the rounds. Blackrock boss Larry Fink, for example, has joined the chorus of cautioners. Companies are already starting to redesign their supply chains, Fink recently told the Financial Times.

But how networked are globally active companies and what conclusions can be drawn from this? This is a question that, in addition to corporate boards, is certainly also increasingly occupying investors, or at least it should.

When exactly the age of globalisation began is a matter of considerable debate. Perhaps it would be Solomonic to claim that there have been several spurts of globalisation in history. Even in Augustus' time, the Roman Empire was engaged in lively trade that reached as far as India. The last big push so far began with the fall of the Berlin Wall and the simultaneous, though unrelated, economic opening of China under Deng Xiaoping, who, among other things, reopened the Shanghai Stock Exchange in 1990. A shift of production began, mainly to Asia, where companies from the industrialised nations not only found cheaper wages and other conditions that were "good" for employers, but also cheaper materials. The high margins of well-known technology and sporting goods manufacturers also stem from this networking.

But if international, widely ramified supply chains with simultaneous low stockholding ("just in time") get out of balance, as in the times of Corona, then this has negative consequences. The shortage inflates the prices of goods. In February, for example, the producer prices of industrial products in Germany rose by an average of 25.9 percent compared to the same month last year - the highest increase since 1949. The war in Ukraine did not play a role in this. And material shortages had already slowed down German industry in 2021, according to the Federal Statistical Office.1

In the USA, producer prices also climbed significantly in February by ten (March: 11.2) per cent compared to the same month last year. The lower increase compared to Germany is probably also due to the United States' lower dependence on foreign supplies. According to a study by the Munich-based ifo Institute commissioned by the Konrad Adenauer Foundation, the degree of integration in value chains of the USA to its gross domestic product is 7.0 per cent (imports) and 6.3 per cent (exports). This is only about one third of Germany's dependence on global value chains.2 Nevertheless, a reshoring initiative ("Bringing Manufacturing at Home") has formed in the USA. According to the initiative, around 1,800 US companies recently intended to move their entire business or at least parts of it back home.

It is not only the less price-sensitive, usually smaller or medium-sized companies that are affected; corporations are also losing business and revenue because of the supply disruptions. The toy manufacturer Hasbro or the substitute meat producer Beyond Meat, for example, recently complained about massively increased freight costs. The sporting goods manufacturer Nike reported failures in Vietnam in autumn 2021 due to strict corona measures. As a result, 160 million fewer shoes went into production.

But how do the ramifications show up in detail? On the basis of ten companies each from the USA and Germany (the aircraft manufacturer Airbus is a French-German hermaphrodite), it is possible to trace the extent of the respective global networking and the dependencies that may have arisen from it. The group can be considered representative. The ten companies from the German share index represent a good 24 percent of the total market capitalisation of all German listed corporations; the ten US companies represent a good eight percent of the market value of all domestic equity securities of the world's heaviest stock exchange. Information on possible dependencies is provided by the business relationships with the ten largest suppliers and customers of each company (in two exceptions the figures are reduced to eight or nine partners).

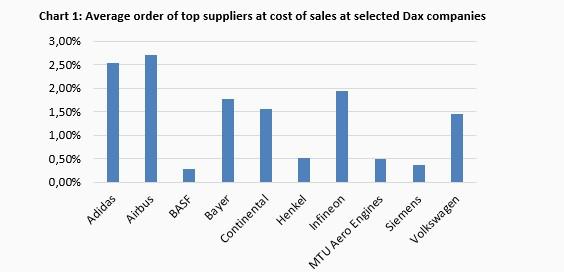

The first thing to note is that the Dax companies are not particularly dependent on their top suppliers, as can be seen from the average volume of orders placed with the most important suppliers at cost of sales (chart 1).

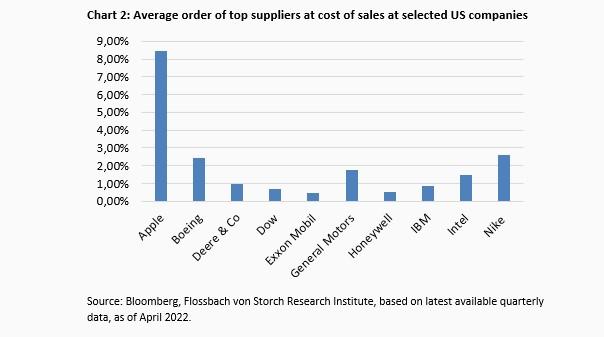

The picture is similar for US companies, with the exception of tech company Apple, which has relatively higher order sizes per top supplier (chart 2).

But where do the orders come from and who are the demanders for the respective companies' end products? Strong domestic demand would suggest that a disruption of international supply chains should affect an overall economy less. In such a case, companies would presumably cope better with deglobalisation, just as a reduction of supply chains should be less burdensome and not as expensive.

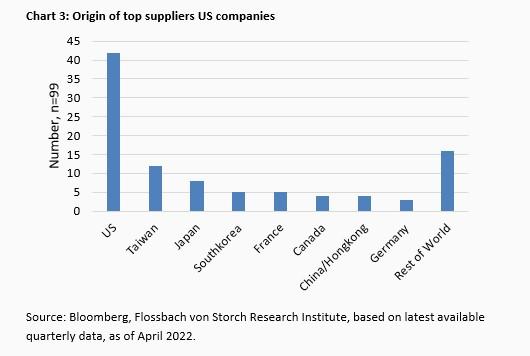

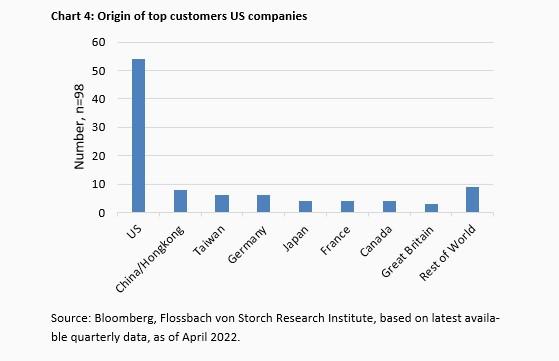

This shows that the USA has clear advantages over Germany. Both the order takers and the customers of US companies are found to a large extent in the domestic market. More than 42 percent of the suppliers and even 54 percent of the customers are American companies (charts 3 and 4).

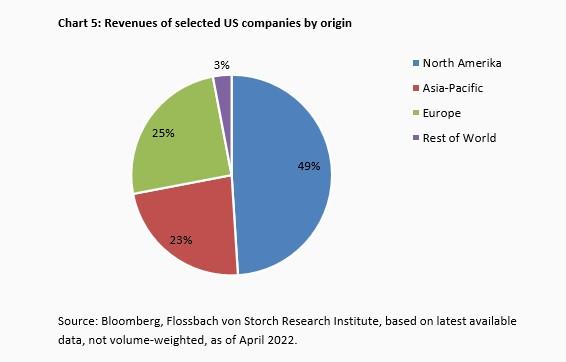

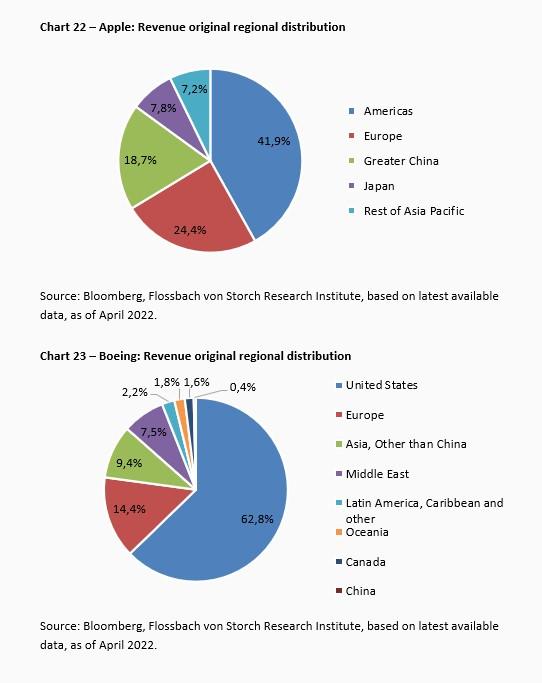

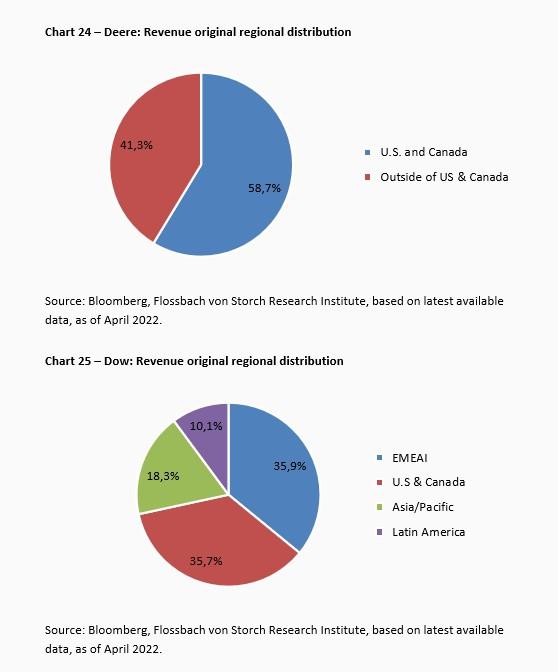

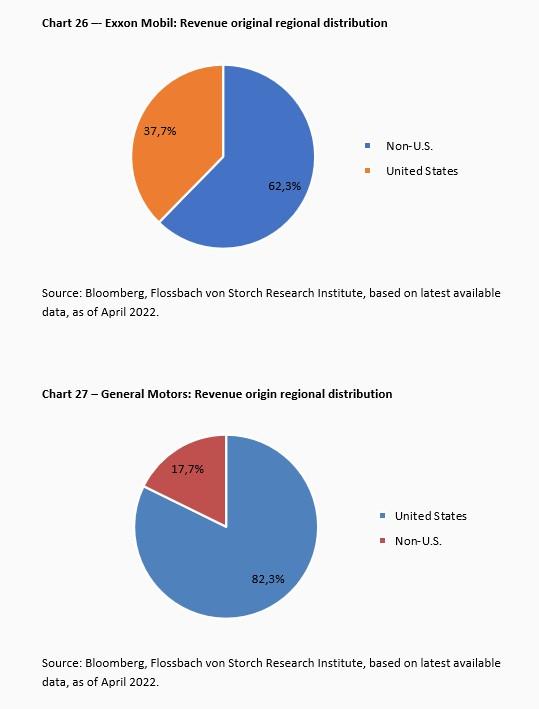

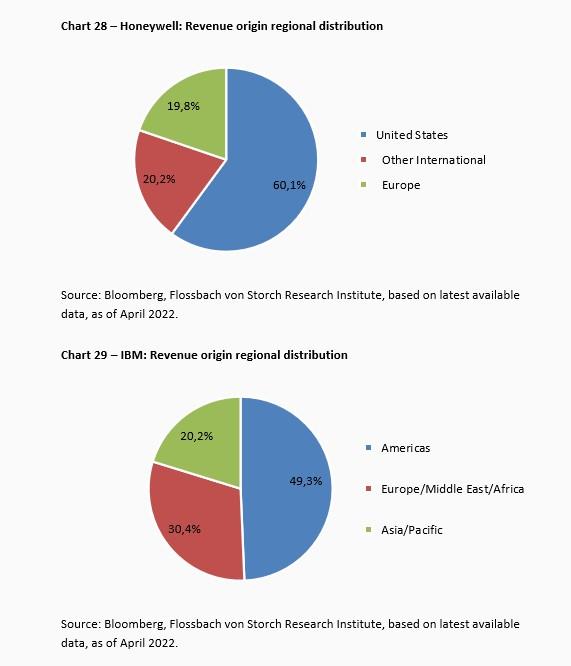

The concentration is also confirmed when all revenues are taken into account. Almost half of the US corporations' revenues come from the USA and Canada (chart 5).

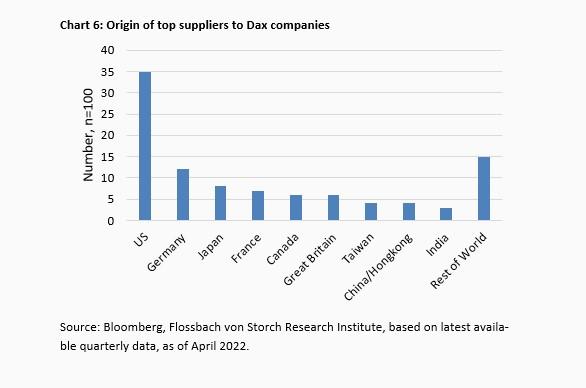

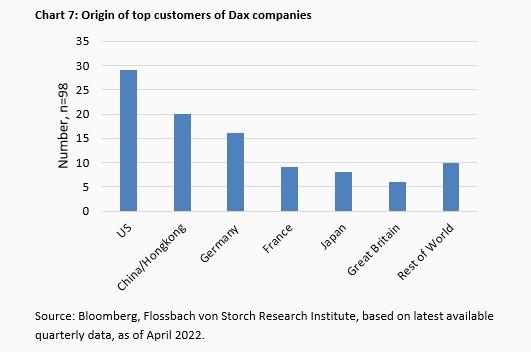

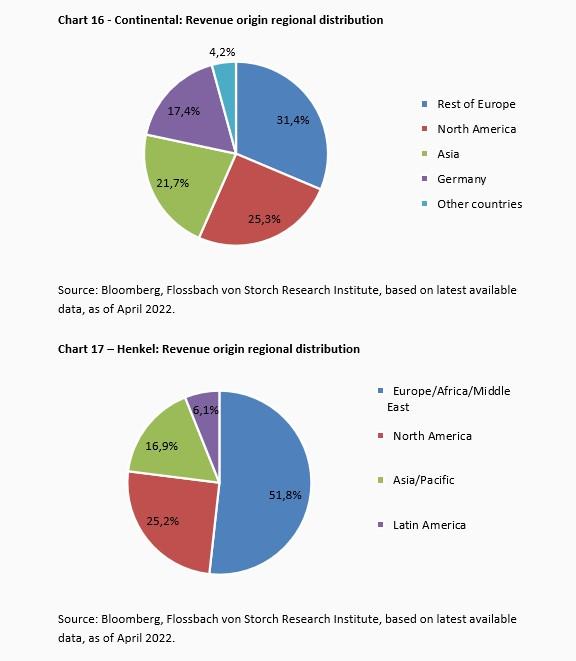

In contrast, the selected Dax companies show themselves to be fundamentally more vulnerable to supply chain difficulties, as they are more foreign-oriented, both in terms of supply and sales. However, in addition to the US companies, which are once again predominant, German, European companies and partners from Canada and Japan play a major role (charts 6 & 7). Thus, the Dax companies are based on a strong "Western bloc".

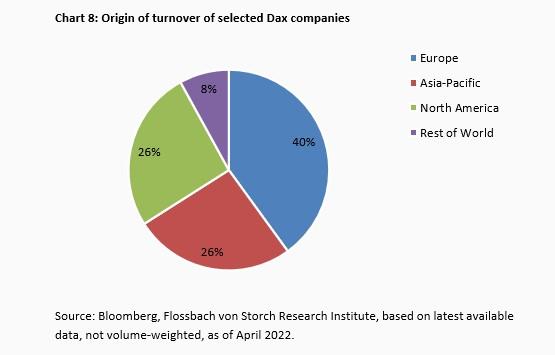

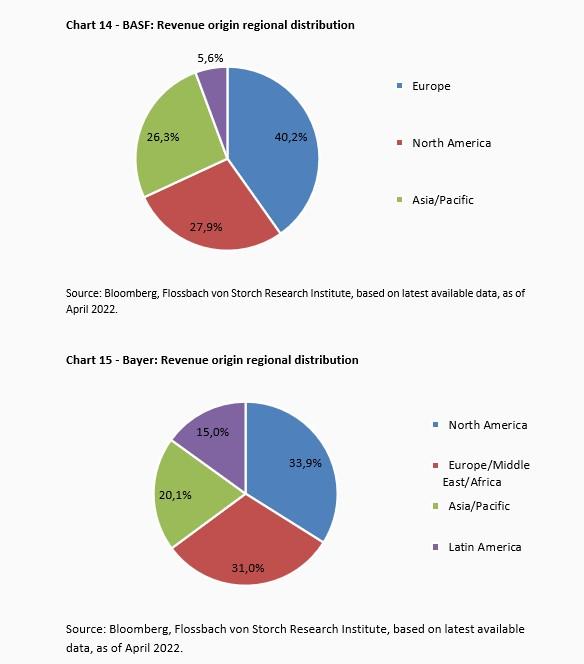

This is also reflected in the distribution of revenues. On average, two-thirds of the revenues of the selected Dax companies come from Europe and North America (chart 8).

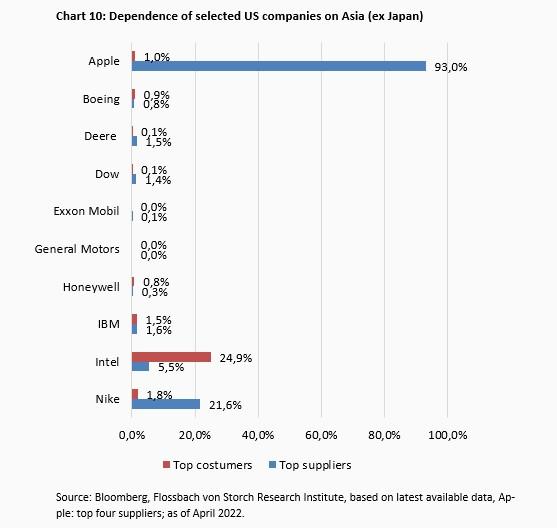

In detail, however, there are major differences. While BASF's most important supplier by volume accounted for only 0.5 per cent of all manufacturing costs of the German chemical company, Apple's top supplier accounted for almost 60 per cent. All of the Californians' most important suppliers come from Asia (Appendix, Tables 1 and 2). In terms of customers, the iPhone manufacturer from California is also much more concentrated than BASF or the German weed killer and pharmaceutical company Bayer, for example. Globalisation is most strongly reflected in Apple. The Californians are more brand owners and designers than producers of hardware; contract manufacturing is the core of their business model. At BASF it is the other way round: the data strongly suggest that the Ludwigshafen-based company has a very high vertical range of manufacture.

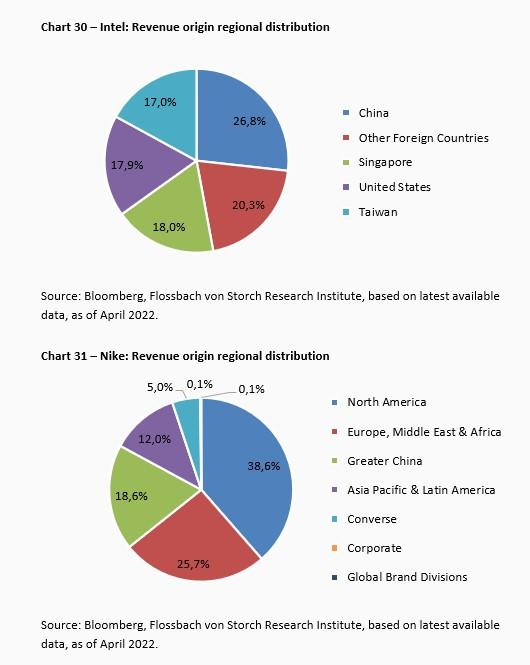

The agricultural machinery manufacturer Deere and the Honeywell Group, known for its ventilation systems, can rely on a solid home base both on a supplier and customer basis. Exxon Mobil has very little dependence on individual customers; the opposite is true of the semiconductor manufacturer Intel.

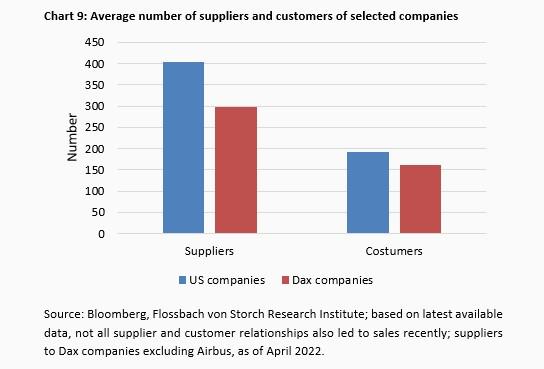

In terms of sheer numbers, US companies are less dependent on suppliers than their Dax counterparts. The selected US companies have on average about one-third more suppliers and almost one-fifth more customers than the Dax companies (chart 9). Airbus, with a very high number of suppliers that would have skewed the average of the Dax companies sharply upwards, is isolated in this regard.

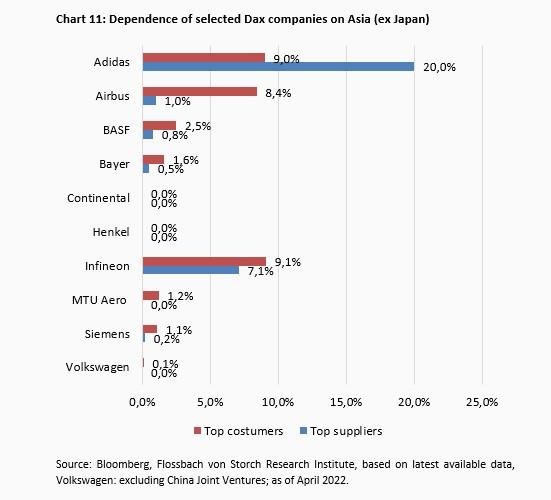

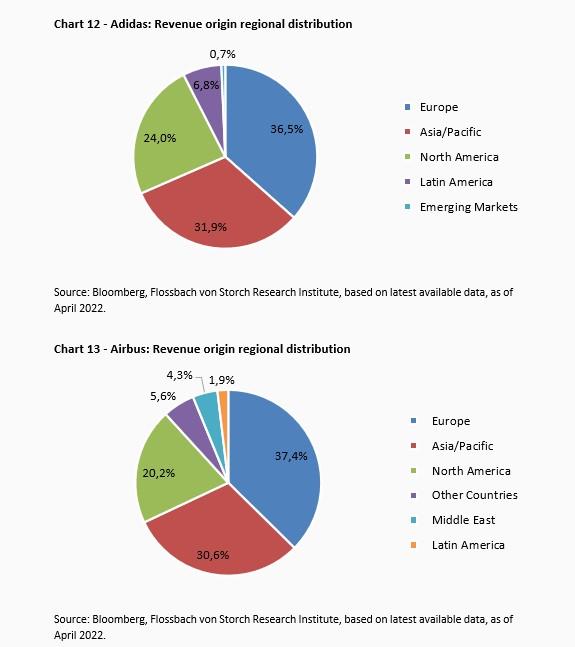

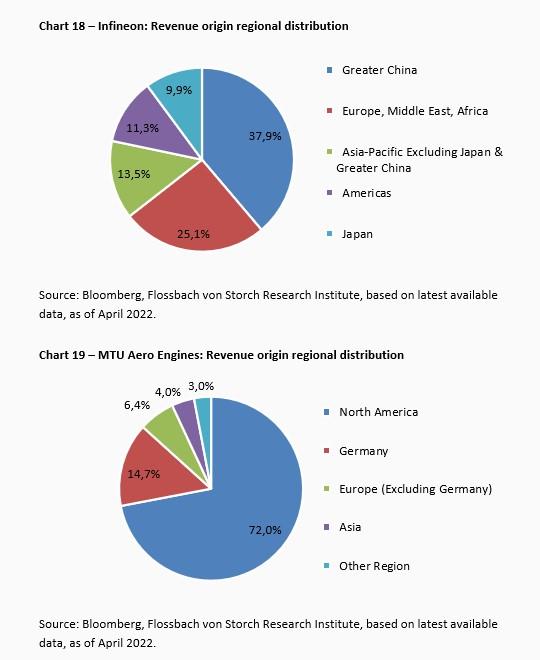

Twins, because both highly dependent on supplies from Asia and with a concentrated customer base, are the sporting goods producers Nike and Adidas. The automotive supplier Continental and the semiconductor manufacturer Infineon are also rather concentrated with a below-average number of suppliers and customers. However, Continental is completely independent of Asia (ex Japan) in terms of its main suppliers and customers. At Infineon, on the other hand, Asia plays a weighty role in terms of both suppliers and customers. The situation is similar for Intel (charts 10 and 11).

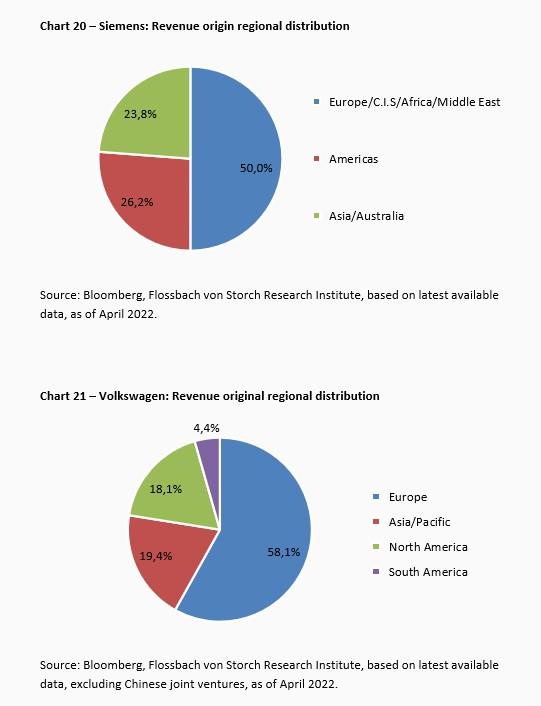

At first glance, the data on Volkswagen, which indicate a low dependence on China (Table 2 and Chart 11), are surprising. However, the overview at VW is incomplete, as the Wolfsburg-based company accounts for its China business, which is largely split into joint ventures, at equity3 - and the (considerable) sales with the Middle Kingdom are therefore not included.

All selected companies rely on a broad supplier base and supply a large number of customers. However, there is a wide range from low to high or higher dependence on individual suppliers and customers. US companies rely primarily on their home market, whereas German companies are mainly active outside their home country. But the western industrialised nations plus Japan are still important for Dax companies.

Overall, the United States is in a superior position. China (including Hong Kong and plus Taiwan) is primarily in demand as a supplier market, less as a sales market (an exception is certainly the German car industry, which needs to be considered in isolation). Overall, the trade of both the US companies and the Dax groups is regionally based on relatively few countries, measured by the respective top suppliers and top customers, so that one can speak of a hub of relations between Germany, France, Great Britain, North America, Japan and China/Hong Kong/Taiwan.

Due to a weaker domestic base, deglobalisation would probably hit German companies harder and lead to higher costs than would be the case for American companies. However, the most valuable company in the world on the stock market - Apple - is highly dependent on its Asian suppliers. This also applies in the opposite direction.

There is no doubt that the difficulties of the past two years will bring a new and special focus to supply chains. This is true for company managers as well as investors. From an investor's perspective, US companies are once again playing out their role as a safe haven due to their strong home base. In addition to the regional connections and concrete corporate linkages presented here, an analysis of the availability of important raw materials and parts was certainly also included - both to be able to assess the individual risks of a company and the probabilities of a possible substitution of the goods.

The problems may be great at present, but deglobalisation is likely to be very difficult or impossible in terms of product availability at affordable prices, which would then be in question. This is shown by the far-reaching networking and the resulting dependencies. From the point of view of many companies, time may dictate that improvements be made in important areas, such as considering increased intermediate storage of important components. However, the question may also be asked to what extent it is in the interest of the companies involved on all continents to actually reverse a decades-long development, which has had a positive effect on profits, but also on consumer prices and employment, in a strong and cost-intensive way.

Globalisation may have passed a certain peak for the time being, but the current phase of a possible review of supply chains is unlikely to mean the end of all relationships. So it goes for Rossell India and its liaison with Boeing. At the end of February, the Indian company received an order to manufacture and supply cable harnesses for the T-7A Red Hawk training jet.

1www.destatis.de/DE/Themen/Wirtschaft/Konjunkturindikatoren/lieferketten.html

2www.kas.de/de/analysen-und-argumente/detail/-/content/globale-wertschoepfungsketten

3 In the case of full consolidation, all relevant balance sheet items of a subsidiary are fully included in the figures of a controlling company. In the case of associated subsidiaries, the at-equity method is applied. In each case, only the share of profit (after tax) of the participation is included; in addition, the parent company's share of the net assets is taken into account. Sales revenues are therefore not reflected in the profit and loss account (of a parent company) - as is the case with Volkswagen's Chinese joint ventures.

28.09.2021 - Macroeconomics

06.12.2019 - Economics, Politics & Philosophy

Where does the strategic rivalry between China and the USA lead?

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann